info@allaroundtexasroofing.com

info@allaroundtexasroofing.com

Schedule Now

Schedule Now (469) 598-0899

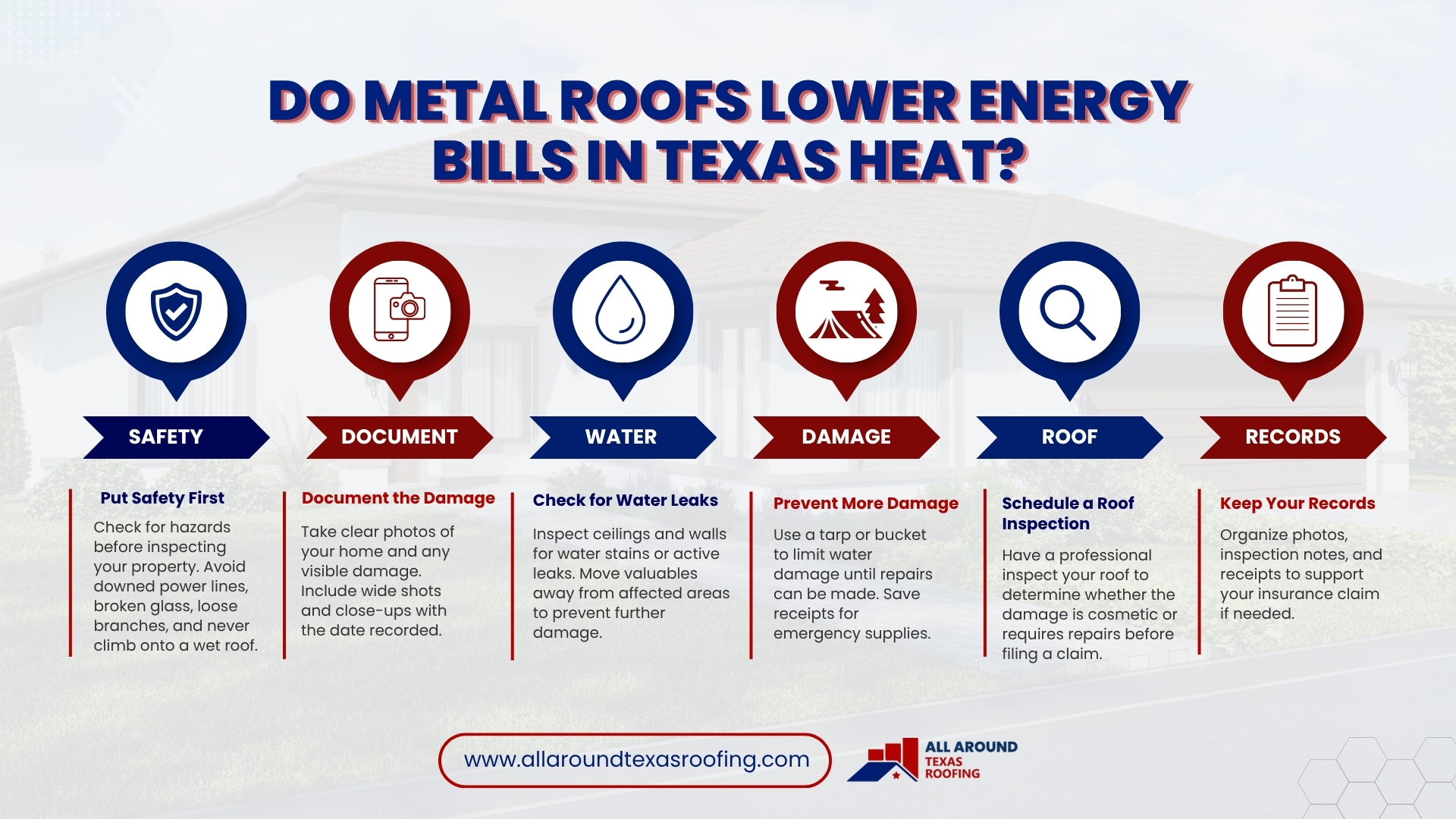

(469) 598-0899Right after a hailstorm, do three things. First, wait until the weather clears and check for safety issues like downed power lines, then look for water spots on ceilings and dented gutters or vents from the ground. Second, take dated photos of everything you can safely see, including damaged siding, fences, and any hail still on the ground. Third, call a licensed roofer for a hail damage roof inspection before you call your insurance company, so you know what you are actually dealing with. Good hail damage roof repair in Texas starts with documentation and a real inspection, not a rushed claim. Roof bruising from hail is often invisible from the driveway, so a trained eye matters. Move quickly, because Texas insurance policies have filing deadlines, and many roofers book solid after a big storm. The steps below walk through each one in plain language.

Was That Storm Actually Bad Enough to Damage My Roof?

Maybe, and the only honest answer is that you cannot always tell from the ground. Hail the size of a quarter or larger can bruise asphalt shingles, and wind gusts over 50 mph can lift or crease them. North Texas sits in one of the most active hail zones in the country, so storms that feel routine can still do real harm. A roof can look fine from the street while the protective granules have been knocked loose, which shortens its life and invites leaks months later.

What you felt and heard during the storm gives you clues. Loud, repeated impacts on the roof, hail piling up on the lawn, or dents showing up on your car and AC unit all point to roof storm damage worth checking. If your neighbors are getting inspections, that is a sign the storm cell passed over your block, too. The safest move is a quick look from the ground, then a closer inspection by someone who climbs up and knows what bruising looks like.

Hail size is a useful gauge, but it is not the whole story. Pea-sized hail rarely hurts a roof in good shape, yet dime to nickel hail driven by hard wind can still strip granules on an older or sun-baked roof. Once you reach quarter-sized stones, most asphalt roofs start taking real hits, and golf-ball or larger hail can crack shingles outright. The age and condition of your roof change the math, too: a roof past 12 to 15 years has brittle shingles that bruise and split far more easily than a newer one. A storm that leaves a five-year-old roof untouched can end the life of one already near retirement. That is why two houses on the same street can come out of the same storm with very different damage.

What Are the First Steps Right After a Hailstorm?

Take care of safety, then start documenting. Those are the first two moves, and they matter more than rushing to call anyone.

Once the storm passes, walk your property carefully. Watch for downed lines, broken glass, and loose branches before you look up at the roof. Check inside for water stains on ceilings or walls, since those signal that water is already getting in. Do not climb on a wet or steep roof yourself, because falls are the real danger after a storm, not the hail.

Next, grab your phone and start photographing. Capture wide shots of the house and close-ups of anything dented or torn. Hit the gutters, downspouts, window screens, fence panels, and any wood siding with hail damage you can reach. A dented gutter or a cracked fence picket is easy proof that hail came down hard. Note the date and time, since most phones tag photos automatically. This early record protects you later if an adjuster questions how recent the damage is.

If you find an active leak, slow the water before it spreads. A tarp weighted at the edges or a bucket under a drip buys you time without putting you on the roof. Move furniture and electronics out from under a ceiling stain, and poke a small hole in any bulging, water-filled drywall so it drains in one spot instead of collapsing across the room. Keep the receipt for the tarp or any supplies, because reasonable emergency steps to limit damage are usually reimbursable once your claim is open.

After safety and photos, line up a roof inspection. A roofer can tell you whether the damage is cosmetic or structural before you file anything, which keeps you from opening a claim you do not need or skipping one you do.

How Do I Spot Hail Damage, and What Is Just Cosmetic?

Look for knocked-off granules, soft bruised spots, and dents on metal, and treat anything that breaks the surface as real. The split between functional and cosmetic damage decides whether your roof needs repair.

On asphalt shingles, hail leaves round dark spots where the granules are gone, and the asphalt underneath shows through. Press one gently, and it may feel soft, like a bruise on an apple. That bruising is functional damage because it exposes the mat and speeds up aging. Cracked or split shingles also count. Cosmetic damage, by contrast, is surface scuffing that does not affect how the roof sheds water, like minor scratches on certain tile finishes.

Metal parts tell the clearest story. Dents in gutters, vents, flashing, and the metal cap on your chimney show the size and force of the hail. If those are dented, your shingles took hits too. For homes with specialty tiles, such as woodland grey roof tiles or other concrete and clay products, cracks and chips are the warning signs rather than granule loss.

Here is a quick field guide:

- Granule loss exposing black asphalt: functional, needs attention

- Soft bruised spots that dent under light pressure: functional

- Cracked, split, or missing shingles: functional

- Dented gutters, vents, and flashing: evidence of impact

- Light surface scuffs that still shed water: often cosmetic

- Cracks or chips on tile: functional, especially if pieces are loose

A few patterns get mistaken for hail and can muddy a claim. Blistering, where small bubbles pop and leave shallow craters, comes from trapped moisture or heat, not impact, and an adjuster will spot the difference. Granules washing into the gutter over the years is normal wear, while sudden bare patches in a random scatter point to a recent storm. Foot traffic from a prior repair leaves shiny, flattened marks in lines rather than the round, random hits hail makes. Knowing these apart before the adjuster arrives keeps the conversation focused on the damage that actually counts.

What Are the Insurance Claim Basics for Texas Roofs?

Document the damage, know your policy, and file within your deadline. A roof insurance claim in Texas follows a fairly standard path once you understand the pieces.

Start by reading your policy declarations page. Look for your deductible, whether you have replacement cost value or actual cash value coverage, and any wind and hail exclusions or separate deductibles, which are common in hail-prone parts of the state. Replacement cost coverage pays to replace your roof at today’s prices minus your deductible, while actual cash value subtracts depreciation, which can leave a bigger gap.

That gap can be large. Say a new roof costs $14,000, and your deductible is $3,000. With replacement cost coverage, the insurer typically pays the first installment minus depreciation, then releases the held-back depreciation once the work is done and invoiced, leaving you out of pocket only for the deductible. With actual cash value on a ten-year-old roof, depreciation alone might knock $5,000 or more off the payout, and that money never comes back. Reading which type you carry before a storm hits tells you what to budget for.

When you file, your insurer assigns an adjuster who inspects the roof and writes an estimate. This is where your early photos and your roofer’s inspection report pull their weight. Many homeowners ask their roofer to be present during the adjuster’s visit so nothing gets missed. Keep a simple file with your claim number, the adjuster’s name, every email, and copies of all estimates.

A few things that help your claim go smoothly:

- File promptly, since Texas policies often require notice within a set window after the storm

- Keep receipts for any emergency repairs, like a tarp to stop a leak

- Do not authorize a full replacement before the claim is settled

- Get the scope of work in writing so the repair matches what was approved

If the first estimate comes back low or denies damage you can plainly see, you are not stuck. You can request a re-inspection, supply your roofer’s measurements and photos, and ask the insurer to send a different adjuster. Texas also lets you invoke the appraisal clause in most policies when you and the insurer disagree on the dollar amount, which brings in independent appraisers to settle the amount. Most disputes get resolved well before that step once the documentation is solid.

Working through a claim feels like a lot, so we put together a step-by-step guide to filing a roof insurance claim in North Texas that breaks down each stage. The goal is a fair payout that actually covers the work your roof needs.

Why Does the Timing of My Inspection Matter So Much?

Because waiting costs you on three fronts: hidden leaks, claim deadlines, and roofer availability. A fast hail damage inspection is the single best thing you can do after a storm.

Damage that looks minor can let water seep into the decking and attic over the following weeks. By the time a ceiling stain appears, the repair may have grown from shingles into wood rot and insulation. An early inspection catches the small problems before they turn into big ones.

Insurance is the second clock. Texas policies set time limits for reporting hail and wind damage, and an old claim is easier for an insurer to question. Getting inspected within days of the storm gives you a dated report that ties the damage to a specific event. Many Texas policies allow a year or more to file, but waiting that long invites trouble: a later storm can muddy which event caused what, and insurers grow skeptical of damage reported long after the fact. A report dated within a week of a known, recorded storm is far harder to dispute.

Then there is simple supply and demand. After a major hailstorm rolls through a Texas county, every reputable roofer’s schedule fills fast. Homeowners who book an inspection early get on the calendar before the rush, while those who wait can sit weeks for the same service. You can read more about working with a contractor after storm damage and what a sound repair process looks like.

How Do I Choose a Roofer Who Won’t Disappear?

Pick a licensed, locally established roofer with real references, and skip anyone who shows up uninvited, demanding a signature. Storm chasers follow hail across the state, do quick work, and vanish before the warranty ever gets tested.

After a big storm, out-of-town crews flood neighborhoods, knocking on doors. Some are fine, but many have no local address, no lasting reputation, and no plan to be around if your roof leaks next year. The pressure tactic of wanting you to sign on the spot is the clearest red flag.

Here is what a roofer who plans to stick around looks like:

- A verifiable local address and phone number, not just a magnet on a truck

- Proof of liability insurance and workers’ compensation

- Written estimates and a clear warranty you can actually read

- Online reviews and references from homeowners in your area

- Willingness to meet your insurance adjuster on site

- No demand for full payment up front before work begins

Pay attention to the warranty details, because not all coverage is equal. A manufacturer’s warranty covers defects in the shingles themselves, while a workmanship warranty covers mistakes the crew makes during installation, which is where most leaks actually start. Ask how many years the workmanship warranty runs and whether it transfers if you sell the house. A roofer who stands behind the labor for five or ten years is making a different promise than one who points only to the shingle maker.

Be careful with any offer to waive or absorb your deductible, since that practice is illegal in Texas and a sign that the contractor cuts corners elsewhere. Ask how long the company has worked in your county and whether they handle the full job, including related work like gutter installation when hail dents the existing ones. A roofer comfortable with Texas roof repair of all sizes, from a few cracked shingles to a full storm replacement, is one you can call again.

Storm damage rarely stops at the roof. The same hail and wind that bruise shingles also leave a wind-damaged fence, dented siding, and torn screens. A roofer who looks at the whole picture helps you document every part of the loss for your claim instead of leaving money on the table.

Ready to Know Exactly Where Your Roof Stands?

After a Texas hailstorm, the smartest first move is a clear-eyed inspection from people who live and work here. At All Around Texas Roofing, we walk the roof, show you the photos, and explain what is functional damage and what is not, so you can decide on repairs and an insurance claim with real information in hand. Reach out while the storm is fresh, your photos are dated, and the inspection calendar still has room.