info@allaroundtexasroofing.com

info@allaroundtexasroofing.com

Schedule Now

Schedule Now (469) 598-0899

(469) 598-0899After a major hailstorm rolls through North Texas, the same question pops up again and again: Will my homeowners’ insurance actually pay for a new roof?

The short answer is yes, in many cases it will. But the longer answer is where things get interesting.

Insurance coverage for roof replacement in Texas depends on how the damage happened, what type of policy you carry, how your deductible works, and even how old your roof is. Two neighbors on the same street can have completely different payouts for similar damage. That surprises a lot of homeowners, especially those dealing with roofing in Prosper TX after recent storms.

If you’re thinking about filing a roof insurance claim in Texas, or you’re just trying to understand your coverage before the next storm hits, this guide will walk you through what really matters.

What Texas Homeowners Insurance Usually Covers

Most standard homeowners policies in Texas are based on what’s called an HO-3 form. Under that type of policy, your roof is typically covered when damage is caused by a sudden and accidental event.

That includes things like:

- Hail damage

- Wind damage

- Falling trees or debris

- Severe storm impact

If a hailstorm cracks shingles or high winds tear them off, that type of damage is usually covered. The insurance company pays to repair or replace the damaged portions of the roof, minus your deductible.

What is not covered? Gradual wear and tear. If your shingles are curling because they’re 20 years old, that’s maintenance, not storm damage. Insurance won’t pay for a roof simply because it’s aging.

In North Texas cities like Prosper, Celina, Frisco, McKinney, Anna, and Melissa, hail claims are extremely common. Our weather patterns make roof damage a regular issue. That’s why understanding your specific policy matters so much.

Why ACV vs. RCV Roof Coverage Changes Everything

One of the biggest factors in how much insurance will pay for your roof replacement in Texas is whether your policy uses ACV or RCV coverage.

Let’s break that down in plain language.

Replacement Cost Value (RCV)

RCV coverage pays what it costs to replace your roof with similar materials at today’s prices. It does not subtract depreciation for age.

If your roof costs $20,000 to replace and your deductible is $5,000, the insurance company pays the remaining $15,000. That’s straightforward.

RCV policies usually pay in two steps:

- An initial payment is made after the claim is approved.

- A second payment after the work is completed, covering any withheld depreciation.

This structure catches some homeowners off guard, but it’s normal for RCV claims.

Actual Cash Value (ACV)

ACV coverage works differently. It subtracts depreciation based on your roof’s age and condition.

Let’s say your 15-year-old roof would cost $20,000 to replace today. The insurance company might calculate that it has already lost half its value due to age. In that case, they may only pay around $10,000 before your deductible is applied.

If you have a $5,000 deductible, that leaves you with only $5,000 from insurance. The remaining cost comes out of pocket.

ACV vs RCV roof coverage is often the difference between manageable costs and a major financial hit. Over the past several years, more Texas insurers have shifted older roofs to ACV coverage, especially in hail-prone areas.

If you’re not sure which one you have, pull out your declarations page or call your agent before filing a claim.

Wind and Hail Deductibles in Texas: The Number That Surprises Everyone

Another common shock for homeowners is the wind and hail deductible.

In many Texas policies, wind and hail damage have a separate deductible from other types of claims. Instead of being a flat dollar amount, it’s often a percentage of your home’s insured value.

For example:

- Home insured value: $400,000

- Wind and hail deductible: 2%

- Out of pocket before insurance pays: $8,000

That number isn’t based on what the roof costs. It’s based on the value of the home.

Some policies use 1 percent. Others use 2 percent or higher. A few even go up to 3 percent in high-risk storm areas.

When homeowners ask, “Will insurance pay for my roof?” the real answer usually starts with, “What’s your deductible?”

Understanding that number ahead of time helps you plan. It also prevents frustration when the claim settlement arrives.

Roof Payment Schedules: A Growing Trend in Texas Policies

Over the last several years, many insurers in Texas have introduced roof payment schedules.

This means your payout is tied directly to the age of your roof, even if you carry RCV coverage.

A sample schedule might look like this:

- Roof under 5 years old: 100 percent of replacement cost

- Roof 6 to 10 years old: 80 percent

- Roof 11 to 15 years old: 60 percent

- Roof over 15 years old: 50 percent

These percentages vary by carrier, but the concept is becoming more common.

So even if a storm causes full roof damage, the policy may limit how much the insurer pays. That’s something many homeowners only discover after filing a hail damage claim in Texas.

Again, this is why reviewing your policy before storm season matters.

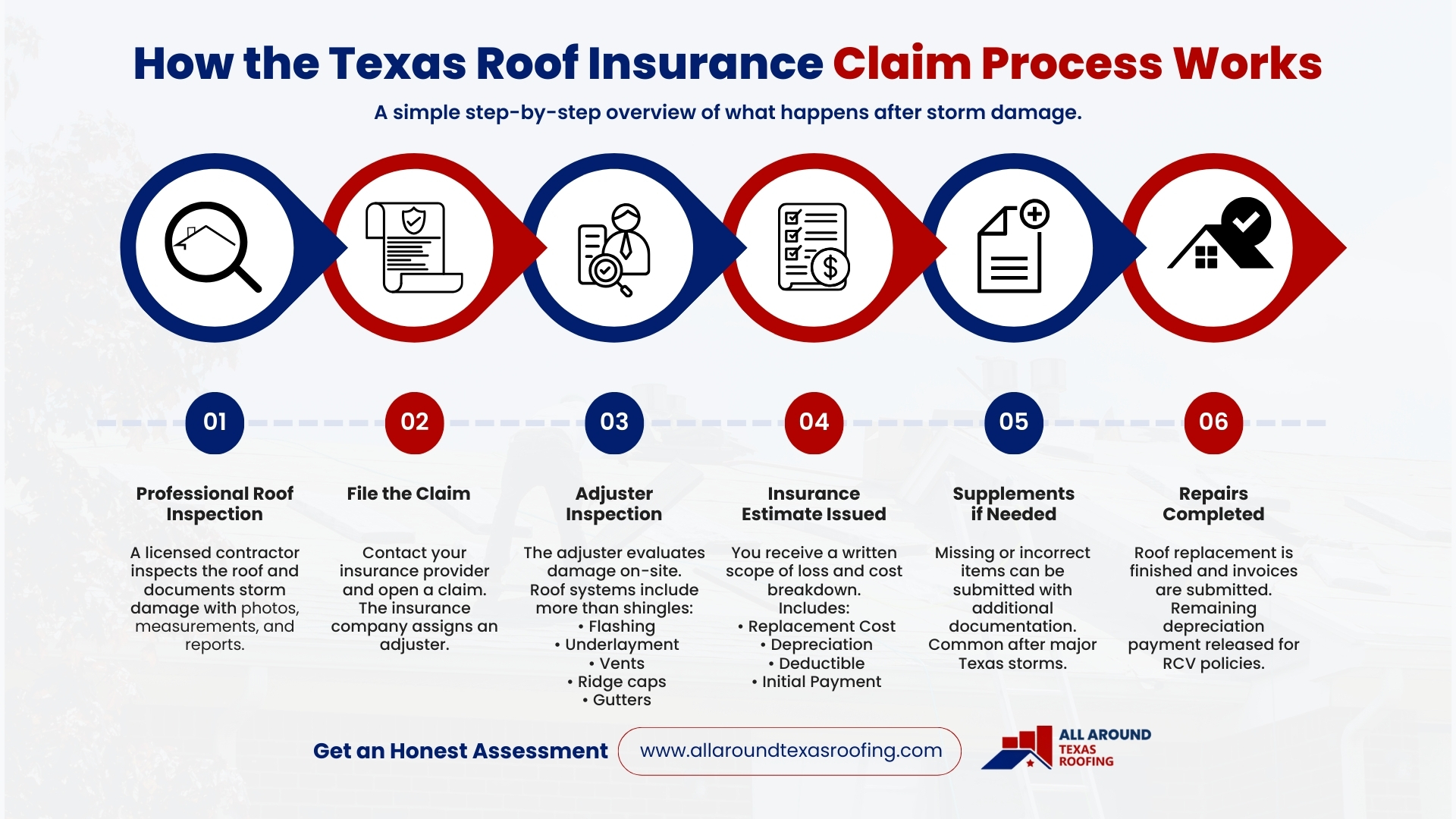

How the Texas Roof Insurance Claim Process Works

If you suspect storm damage, here’s how the process typically unfolds.

1. Schedule a Professional Inspection

Start with a detailed roof inspection from a licensed roofing contractor who understands storm damage documentation. Photos, measurements, and written reports are critical.

This inspection determines whether filing a claim makes sense. Not every roof needs replacement after a storm.

2. File the Claim

If damage is confirmed, you contact your insurance company and open a claim. They assign an adjuster.

3. Adjuster Inspection

The adjuster visits your property to inspect the damage. This is where many claims are won or lost. If certain components are overlooked, they won’t be included in the estimate.

Roofing systems are more than shingles. Flashing, underlayment, ridge caps, vents, gutters, and even interior damage may need attention.

4. Insurance Estimate Issued

The insurance company sends a written scope of loss and payment breakdown. This shows:

- Replacement cost

- Depreciation

- Deductible

- Initial payment

Review this carefully. Mistakes can happen.

5. Supplements if Needed

If items are missing or priced incorrectly, a supplemental claim can be submitted with additional documentation. This is common in Texas roof insurance claims, especially after large storm events.

6. Work Completed and Final Payment Released

Once the roof replacement is finished and invoices are submitted, the remaining depreciation is released for RCV policies.

Why Documentation Makes or Breaks a Claim

Storm claims aren’t just about damage. They’re about proof.

Clear photos of hail strikes, lifted shingles, and collateral damage matter. Manufacturer specifications matter. Local building codes matter.

North Texas cities often require specific upgrades when replacing a roof, such as updated flashing or ventilation adjustments. Insurance estimates should reflect those requirements.

When documentation is weak, claims get reduced or denied. When documentation is thorough, outcomes tend to be smoother.

Common Reasons Roof Claims Get Denied in Texas

While most storm-related claims are approved, denials do happen.

Here are some typical reasons:

- Damage is determined to be wear and tear rather than storm-related

- The policy excludes cosmetic damage

- The roof is past a certain age threshold

- Coverage had been switched to ACV

- The deductible exceeds the estimated damage

Sometimes a denial is final. Other times, additional evidence can change the outcome.

If your claim is denied, ask for the written explanation. Understanding the reasoning helps determine next steps.

How to Prepare Before the Next Storm

You can’t control Texas weather. You can control how prepared you are.

A few simple steps help:

- Review your policy annually

- Confirm whether you have ACV or RCV coverage

- Check your wind and hail deductible percentage

- Ask if a roof payment schedule applies

- Keep maintenance records

These small actions can save a lot of stress later.

Many homeowners only review their policy after damage occurs. By then, options are limited.

Local Storm Patterns in North Texas

Communities across Collin County and Denton County experience frequent hail and wind events. Spring and early summer storms often produce large hail capable of shortening a roof’s lifespan dramatically.

Insurance carriers track claims by ZIP code. High claim frequency can influence future policy changes, including deductible increases or ACV endorsements.

That’s another reason many homeowners in cities like Frisco and McKinney schedule regular checkups with a local residential roofing service to review their roof’s condition before minor issues turn into major insurance claims.

Choosing the Right Contractor for Insurance Work

Not all roofing contractors handle insurance claims the same way.

When selecting a contractor for a roof insurance claim in Texas, look for:

- Experience working with adjusters

- Detailed inspection reports

- Knowledge of local building codes

- Clear communication about deductible and payment steps

A contractor should explain the process without pressure or unrealistic promises. No one can legally waive your deductible. Be cautious of anyone who claims they can.

Getting Help With Insurance Claim Assistance

Storm damage can feel overwhelming. There’s paperwork, inspections, and conversations with adjusters. It’s a lot to manage when you’re already dealing with property damage.

All Around Texas Roofing and Restoration provides Insurance Claim Assistance for homeowners across Prosper, Celina, Frisco, McKinney, Anna, and Melissa. From detailed inspections to adjuster meetings and supplemental documentation, the goal is to help homeowners receive the coverage their policy provides without confusion or guesswork.

If you suspect hail or wind damage, scheduling a professional inspection is often the first practical step.

So, Will Insurance Cover Roof Replacement in Texas?

In many cases, yes. If your roof was damaged by hail, wind, or storm debris, your homeowners’ insurance policy will typically cover repair or replacement, minus your deductible and subject to your specific coverage type.

But the details matter. ACV vs RCV coverage, wind and hail deductibles, and roof payment schedules can all change the final payout.

Understanding your policy now is far easier than trying to figure it out after shingles are scattered across your yard.

If you’re unsure about storm damage or how your coverage works, a professional inspection can provide clarity. And when questions come up, having a contractor who understands Texas roof insurance claims makes the process far less stressful.

All Around Texas Roofing and Restoration serves homeowners throughout North Texas and can help guide you through the claim process from inspection to completion.